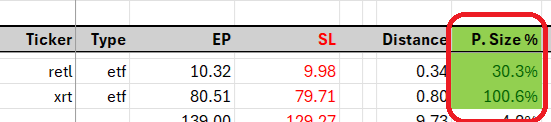

Understanding the Infeasibility of '1% Risk to Equity' and Benefits of High ADR% Securities Your question is excellent, and I’d like to clarify why aiming for a 1% risk-to-equity ratio is often unrealistic due to position sizing constraints. I’ll also compare lower ADR% products, like $XRT at 1.41% ADR, with higher ADR% products, like $RETL at 4.06% ADR (a 3x leverage of $XRT, sharing the same price structure on intraday timeframes). In the example below, I simulate an entry price and stop-loss price based on $XRT and $RETL high and low range and automate the calculation of position size % required for a “1% risk” approach relative to account equity (excluding existing unrealized gains/losses of other positions). Using a 1% risk model, you would need to allocate almost your entire account (without margin) to $XRT and about 30% of your account to $RETL with its higher ADR%. The 1% risk approach may work for traders constraining themselves to securities with ADRs above 5%, as structuring trades based on high/low intraday ranges often only requires 10-25% of equity, enabling a minimum of four concurrent positions on swings. However, with names like $TSLA, $MSFT, or $NVDA, even synthetic leveraged of those names like $TSLL, $MSTU, or $NVDU wouldn’t allow for comfortable positioning. This is no secret if you have the right metrics on your spreadsheet. @stamatoudism have also highlighted about inflexibility of even 0.5% risk in his first interview with @TraderLion_ I suggest starting with a 0.15% risk per trade, increasing only when you begin to see the benefit of having a ADR% cut off in your screening and share structure of higher ADR% securities. Personally, I max out at around 0.33%, especially when most active names now are in the 2b-25b market cap range, with floats below 50 million shares and ADRs above 4.5%. This are the trademark of momentum names, and it make alot of sense why are able to move in such rapid fashion on those share structure. I just wish to add that High ADR% securities offer the benefit of greater intraday range expansion without substantial capital lock-up compared to lower ADR% names. I avoid trading products like $XRT or $TSLA directly, preferring leveraged ETFs when they provide sufficient liquidity for the same reason. It gives you alot of capital excess when a 5-star/A-rated setup in the latter stage of your position building.

Understanding the Infeasibility of '1% Risk to Equity' and Benefits of High ADR% Securities Your question is excellent, and I’d like to clarify why aiming for a 1% risk-to-equity ratio is often unrealistic due to position sizing constraints. I’ll also compare lower ADR% products, like $XRT at 1.41% ADR, with higher ADR% products, like $RETL at 4.06% ADR (a 3x leverage of $XRT, sharing the same price structure on intraday timeframes). In the example below, I simulate an entry price and stop-loss price based on $XRT and $RETL high and low range and automate the calculation of position size % required for a “1% risk” approach relative to account equity (excluding existing unrealized gains/losses of other positions). Using a 1% risk model, you would need to allocate almost your entire account (without margin) to $XRT and about 30% of your account to $RETL with its higher ADR%. The 1% risk approach may work for traders constraining themselves to securities with ADRs above 5%, as structuring trades based on high/low intraday ranges often only requires 10-25% of equity, enabling a minimum of four concurrent positions on swings. However, with names like $TSLA, $MSFT, or $NVDA, even synthetic leveraged of those names like $TSLL, $MSTU, or $NVDU wouldn’t allow for comfortable positioning. This is no secret if you have the right metrics on your spreadsheet. @stamatoudism have also highlighted about inflexibility of even 0.5% risk in his first interview with @TraderLion_ I suggest starting with a 0.15% risk per trade, increasing only when you begin to see the benefit of having a ADR% cut off in your screening and share structure of higher ADR% securities. Personally, I max out at around 0.33%, especially when most active names now are in the 2b-25b market cap range, with floats below 50 million shares and ADRs above 4.5%. This are the trademark of momentum names, and it make alot of sense why are able to move in such rapid fashion on those share structure. I just wish to add that High ADR% securities offer the benefit of greater intraday range expansion without substantial capital lock-up compared to lower ADR% names. I avoid trading products like $XRT or $TSLA directly, preferring leveraged ETFs when they provide sufficient liquidity for the same reason. It gives you alot of capital excess when a 5-star/A-rated setup in the latter stage of your position building.

Last week, I unfollowed someone I once respected after he claimed to trade with a 1.5% risk to equity (via this replies to his followers) and entered $NVDA on the 5/11 ORH setup, while also carrying multiple high flying trades. Literally impossible, total nonsense😅

Use this as a reference: the trade entry and stop are structured within a single candle print, based on fixed variables for risk percentage and % of Low-of-Day execution. 1% ADR, (30% LoD execution), 0.3% Risk to Equity = 50% Capital Required 2% ADR, (30% LoD execution), 0.3% Risk to Equity = 25% Capital Required 3% ADR, (30% LoD execution), 0.3% Risk to Equity = 12.5% Capital Required 4% ADR, (30% LoD execution), 0.3% Risk to Equity = 6.25% Capital Required

@jfsrevg Nice read. 1% risk per trade should be around the maximum, but that has to be combined with a max position size and personally my max in one position is 22% so 90% of the time your stop is way lower than 1% account risk because of tight stops

Hi Jeff, I want to express my gratitude for your selfless commitment to teaching, which has significantly benefited the trading community. I am facing a somewhat similar issue, but from the opposite angle; I primarily trade options. My goal is to grow my account as quickly as possible while minimizing risk. Like in your example, I also utilize a 1% equity risk. However, as demonstrated in my example below, the net effect on my account is minimal. On a cost basis, this approach uses only 7.8% of my equity. In contrast, trading shares, as you pointed out, would consume 364% of my equity, pushing me into margin territory. I would appreciate your thoughts on how I can achieve my objectives while maintaining a total daily risk level of 3% of equity, thus in this case, limiting myself to no more than three trades per day. Thank you!

@jfsrevg A few of the very best traders I follow prefer higher priced stocks as the entries often gives tighter risk and hence you can have a much higher position size, especially if you trade on Undercut and rallies and similar higher low setups.

@jfsrevg Thanks boss! Appreciate the clear and solid answer! With these type of plays I also have my % risk to equity at the 0.10-0.33% range. Salute!

@jfsrevg Not possible to risk 1% for a trader using super tight stops but very feasible for someone with a wider stop, so for the same price move, a 3RR profit for one could be equivalent to 10RR profit for someone risking 0.33%. The end result is the same (3%~ profit)so it really depends

@jfsrevg Thank you, Jeff, for these interesting threads on risk and position sizing. I am not sure i'm clear about the 0.15% risk and correlation with ADR%. and are you limiting risk per trade at 0.33% regardless of the ADR/ATR?

@jfsrevg Jeff let's make it more simple and scarier for people: IT'S IMPOSSIBLE to trade at 1% risk to equity without using other's people money. Understand margin and protect yourself!

@jfsrevg Trying to understand what you explained. Can I say that our SL should be multiples of ADR%. So if we got with higher ADR% stocks it will increase our SL and hence will be difficult or no advisable to go with 1% risk on capital. Is that correct understanding?