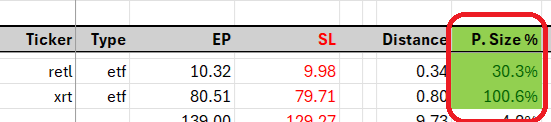

Understanding the Infeasibility of '1% Risk to Equity' and Benefits of High ADR% Securities Your question is excellent, and I’d like to clarify why aiming for a 1% risk-to-equity ratio is often unrealistic due to position sizing constraints. I’ll also compare lower ADR% products, like $XRT at 1.41% ADR, with higher ADR% products, like $RETL at 4.06% ADR (a 3x leverage of $XRT, sharing the same price structure on intraday timeframes). In the example below, I simulate an entry price and stop-loss price based on $XRT and $RETL high and low range and automate the calculation of position size % required for a “1% risk” approach relative to account equity (excluding existing unrealized gains/losses of other positions). Using a 1% risk model, you would need to allocate almost your entire account (without margin) to $XRT and about 30% of your account to $RETL with its higher ADR%. The 1% risk approach may work for traders constraining themselves to securities with ADRs above 5%, as structuring trades based on high/low intraday ranges often only requires 10-25% of equity, enabling a minimum of four concurrent positions on swings. However, with names like $TSLA, $MSFT, or $NVDA, even synthetic leveraged of those names like $TSLL, $MSTU, or $NVDU wouldn’t allow for comfortable positioning. This is no secret if you have the right metrics on your spreadsheet. @stamatoudism have also highlighted about inflexibility of even 0.5% risk in his first interview with @TraderLion_ I suggest starting with a 0.15% risk per trade, increasing only when you begin to see the benefit of having a ADR% cut off in your screening and share structure of higher ADR% securities. Personally, I max out at around 0.33%, especially when most active names now are in the 2b-25b market cap range, with floats below 50 million shares and ADRs above 4.5%. This are the trademark of momentum names, and it make alot of sense why are able to move in such rapid fashion on those share structure. I just wish to add that High ADR% securities offer the benefit of greater intraday range expansion without substantial capital lock-up compared to lower ADR% names. I avoid trading products like $XRT or $TSLA directly, preferring leveraged ETFs when they provide sufficient liquidity for the same reason. It gives you alot of capital excess when a 5-star/A-rated setup in the latter stage of your position building.

Understanding the Infeasibility of '1% Risk to Equity' and Benefits of High ADR% Securities Your question is excellent, and I’d like to clarify why aiming for a 1% risk-to-equity ratio is often unrealistic due to position sizing constraints. I’ll also compare lower ADR% products, like $XRT at 1.41% ADR, with higher ADR% products, like $RETL at 4.06% ADR (a 3x leverage of $XRT, sharing the same price structure on intraday timeframes). In the example below, I simulate an entry price and stop-loss price based on $XRT and $RETL high and low range and automate the calculation of position size % required for a “1% risk” approach relative to account equity (excluding existing unrealized gains/losses of other positions). Using a 1% risk model, you would need to allocate almost your entire account (without margin) to $XRT and about 30% of your account to $RETL with its higher ADR%. The 1% risk approach may work for traders constraining themselves to securities with ADRs above 5%, as structuring trades based on high/low intraday ranges often only requires 10-25% of equity, enabling a minimum of four concurrent positions on swings. However, with names like $TSLA, $MSFT, or $NVDA, even synthetic leveraged of those names like $TSLL, $MSTU, or $NVDU wouldn’t allow for comfortable positioning. This is no secret if you have the right metrics on your spreadsheet. @stamatoudism have also highlighted about inflexibility of even 0.5% risk in his first interview with @TraderLion_ I suggest starting with a 0.15% risk per trade, increasing only when you begin to see the benefit of having a ADR% cut off in your screening and share structure of higher ADR% securities. Personally, I max out at around 0.33%, especially when most active names now are in the 2b-25b market cap range, with floats below 50 million shares and ADRs above 4.5%. This are the trademark of momentum names, and it make alot of sense why are able to move in such rapid fashion on those share structure. I just wish to add that High ADR% securities offer the benefit of greater intraday range expansion without substantial capital lock-up compared to lower ADR% names. I avoid trading products like $XRT or $TSLA directly, preferring leveraged ETFs when they provide sufficient liquidity for the same reason. It gives you alot of capital excess when a 5-star/A-rated setup in the latter stage of your position building.

Use this as a reference: the trade entry and stop are structured within a single candle print, based on fixed variables for risk percentage and % of Low-of-Day execution. 1% ADR, (30% LoD execution), 0.3% Risk to Equity = 50% Capital Required 2% ADR, (30% LoD execution), 0.3% Risk to Equity = 25% Capital Required 3% ADR, (30% LoD execution), 0.3% Risk to Equity = 12.5% Capital Required 4% ADR, (30% LoD execution), 0.3% Risk to Equity = 6.25% Capital Required

@jfsrevg Hi Jeff, may I ask for any calculation sheet/formula to attain these numbers? Maybe I can change the parameters according to my requirements. Many thanks!